Introduction

Recent events, including the coronavirus pandemic and war in Ukraine, with the ensuing energy crisis and higher inflation, have fundamentally challenged the economic model that had been in place since 2010. But they have not changed the political consensus around popular attitudes to tax – that people hate tax; tax rises are not politically feasible; and that if increases are made they must be in the form of stealth taxes or time-limited.

Tax cuts were a major feature of the Conservative leadership campaign last summer. And although the market response to Liz Truss’s attempt to cut taxes on high-income taxpayers without showing how this would be funded ended up making her the shortest-serving prime minister ever, Tory backbenchers were again pushing Chancellor Jeremy Hunt to cut taxes by the time of the budget in March. The limited (if expensive) tax cut from abolishing the lifetime pension allowance in that budget was given much more prominence than the increases in income tax from freezing thresholds (described in some media reports, not without reason, as a ‘stealth’ increase). And despite recurring and overlapping crises in public services and widespread public sector strikes over pay, there was almost no discussion of how public services could be sustainably funded in the long term. On the other side of the political spectrum Labour leader Keir Starmer recently launched the party’s local election campaign with the promise that Labour was ‘the party of lower taxes for working people’, again promising tax reductions for the majority (if not everyone).

This idea about negative popular attitudes to taxes in general, and to any increases in particular, has a real impact; our current tax system is in part the result of the political belief that the space for tax reform is constrained by long-standing popular opposition. Looking at the actual evidence about popular attitudes to personal taxes in Britain – and how they evolved over the second half of the twentieth century – reveals a far less clear-cut picture.

Evidence for popular attitudes to tax

It is often stated to be a truth universally acknowledged that no one likes paying tax. Edmund Burke’s statement in 1774 that “To tax and to please, no more than to love and be wise, is not given to men” is still quoted. This belief has contributed to inefficiencies and distortions in our tax system – the consistent failure to uprate fuel duty, despite the government’s net zero goal, for example. In the press, discussions of the fact that tax as a percentage of GDP is now at its highest level since the 1970s generally assume that this is inevitably negative and do not discuss tax levels in comparable economies, what kind of services people expect, or the pressure that an ageing population, in particular, is putting on the tax system. A meaningful conversation about what sort of tax regime we want and what that implies for public services – whether we can aspire to Scandinavian levels of public services with American levels of tax – has been hampered by the assumption that tax changes will inevitably be unpopular.

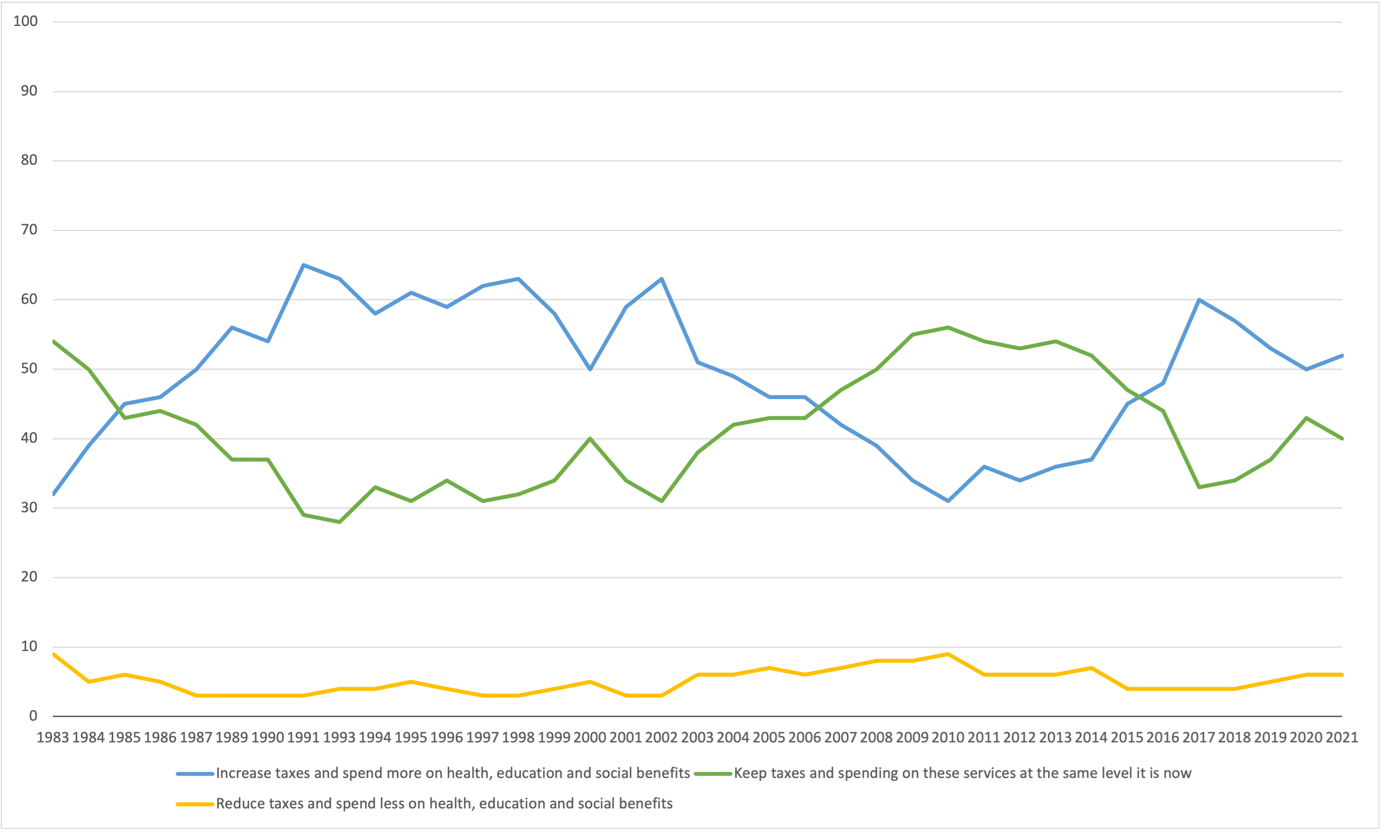

However, contemporary polling shows only a small minority expressing a preference for tax cuts if that also means cuts to services – never above 9% in the authoritative British Social Attitudes survey through the last four decades. For most of those 40 years, including since 2017, an absolute majority have expressed support for an increase in taxes to fund higher spending on health, education, and social benefits.

British Social Attitudes survey, 1983- 2021

Question: Suppose the government had to choose between the three options on this card. Which do you think it should choose? (Blue: increase taxes; Green: keep taxes at the same level; Yellow: reduce taxes)

Source: Butt, S., Clery, E. and Curtice, J., British Social Attitudes: The 39th Report. London: National Centre for Social Research, 2022.

There are legitimate questions about whether these polling findings are representative of real attitudes or whether they are the product of social desirability bias – where respondents want to give the ‘right’ answer. One recent study did suggest that tax increases in an election year reduced re-election rates for incumbent governments but only among some groups of voters, and it did not find a positive impact from tax cuts. There is also some evidence to support the polling – in Milton Keynes in 1999, for example, the council asked voters to choose between a 15% increase in council tax and some extra spending; a 9.8% increase in council tax and no change in spending; or a 5% increase in council tax with some cuts to services such as education. With a turnout of 44.7% (higher than local council elections in the same period) 23.6% voted for the first option, 35% for the second option, and 30.05% for the third option, supporting the idea that under some circumstances voters will choose to maintain or increase spending, even if that requires tax increases.

The British Social Attitudes survey only started in 1983, so what about earlier periods – have attitudes changed over time? It has often been suggested that attitudes towards tax became significantly more negative in the 1970s. But my doctoral research does not support that idea. It examined the archival record for views about popular attitudes to personal taxation in four key political and economic organisations – the Labour and Conservative parties, the TUC, and the FBI (which became the CBI in 1965) – as well as among civil servants in the Treasury and Inland Revenue, at key dates involving general elections or budget statements in the period 1949-92 (1949-51; 1959-61; 1964-65; 1970; 1976; 1979, 1987, 1992). Opinions expressed in a sample of national newspapers – the Daily Express, Daily Herald (-1964), Daily Mail, Daily Mirror, Daily Telegraph, Guardian, Financial Times, Times, and Observer — and major weekly political magazines — the Economist, New Statesman, and Spectator – were also examined at these dates, along with available opinion surveys across the period.

This systematic research finds a very different story. Firstly – and not necessarily surprisingly given the unprecedentedly high levels of taxation brought in during World War II – there was an assumption around 1950 in the organisations studied that such high levels of tax were unpopular and should be reduced if possible, while at the same time that the newly extended public services were very popular. Some evidence of a perception of at least popular acquiescence to high taxation and spending was found around 1960, but only in the press and Conservative party, where some researchers and politicians suggested that people were more concerned about services than tax cuts. Assertions of popular opposition to personal tax rises increased again in these organisations through the 1960s and into the 1970s, but, perhaps most surprisingly, not to a level that was markedly different than that around 1950. And while there was a perception of popular opposition to the increasing level and scope of income tax as inflation rose through the 1970s, this appeared to be seen more as a reaction to short term pressures, than as any fundamental change.

Instead, perceptions of popular opposition to personal tax levels and any increases were consistently balanced by an assumption of support for public services, while the idea of ‘fairness’ was key to ideas about the overall shape and progressivity of the tax system. The overall picture from these different sources of evidence from the late 1950s to the start of the 1990s is one of continuity not change.

The late 1940s and early 1950s

So, the late 1940s and early 1950s do not appear from this evidence as a golden age of popular consensus in favour of high taxation. Discussions in political parties, the civil service, civil society organisations, and the press assumed significant popular opposition to contemporary tax levels, with the press emphasising this particularly strongly. The Guardian, for example, argued in 1949 that the country was ‘groaning under the weight of taxes’ and that ‘demands for relief’ came from all sides. Similarly, the Times referenced a year later ‘the deep, unsatisfied longing of all taxpayers for lower taxes’.

Labour politicians also assumed popular opposition to high tax levels and tax increases. In 1948 the then Labour Chancellor Stafford Cripps said:

Everybody, of course, especially any Chancellor, would absolutely love to remit all the taxes, nothing could make him more popular in the country … I have had that [such complaints] from every single person who has had any increased incidence of tax under this Budget. You always get it.

After Labour’s 1950 election losses, Labour M.P. Anthony Crosland wrote in Tribune that, ‘the most important single issue which caused these people to swing Tory was probably the weight of taxation’. Civil servants working on government economic policy made similar comments – one Inland Revenue memo suggested in 1950 that any increase in income tax would be ‘denounced as a further attack on the middle classes’ and would ‘be no more favourably received by the working man who is already sufficiently vocal about the incidence of income tax on his overtime’. A note by a Conservative party official in 1948 identified tax cuts as the main tool they had for attracting voters:

We cannot reduce prices — we cannot materially increase lower scale salaries — but we can reduce taxation by economies … We must discuss this ad nauseam.

The Federation of British Industries (FBI) emphasised their members’ opposition to tax levels, particularly corporate taxes – Chairman Norman Kipping stated in a letter to a Treasury official in 1949 that a proposed increase in profits taxes had aroused ‘great resentment’ among firms, although FBI officials generally seemed concerned about popular attitudes more widely only in relation to securing wage restraint. TUC officials in 1949-50 also seemed to believe that tax cuts would be popular – TUC headquarters were receiving numerous letters from unions and councils complaining about income tax on overtime (without extra overtime earnings most waged workers would not have earned enough to incur income tax).

At the same time, individuals in all the organisations studied assumed (as in later periods) that there was widespread support for spending on public services and that fairness was a major concern. The TUC suggested tax cuts only as part of a wider range of policies necessary for wage restraint and complaints from members about the 1949 budget generally focused on cost-of-living increases, fairness, and broken promises, rather than the lack of tax cuts. Civil servants at a Budget Committee meeting in 1950 suggested that surtax cuts (benefiting higher earners) could not be introduced without a balancing cut for low earners.

Ideas about popular attitudes in these organisations were rarely obviously based on any empirical evidence. Conservative researchers did disseminate their own commissioned Gallup polling summary in January 1950, reporting that tax cuts were second – behind reducing prices – in ‘the things which would draw the most votes for the Party promising them’. However, tax also continued to come low in lists of major issues; other opinion summaries sent to Conservative Central Office later in the same year, for example, suggested that people did not know, or care, very much about taxation. One stated:

… the following extract of a report from Cheshire illustrates the attitude of many:- “The prospect of increased tax was treated with indifference, the general reaction being that only the rich were affected.”

Whether these reports about popular attitudes were representative is difficult to confirm as almost no independent survey evidence was found from the late 1940s and early 1950s. Two isolated Gallup surveys suggested that respondents were willing to pay higher taxes in return for increased spending on pensions, but the quantitative evidence is too limited to draw any strong conclusions.

What is clear is that the period around 1950 does not appear as a moment of unprecedented popular consent to high tax levels or further tax increases. One could tentatively propose, therefore, that the evidence suggests a situation not so different from that found by 1992 (to be shown below) — politicians and the press emphasising popular opposition to tax, while survey evidence suggested tax cuts in the abstract were popular but that taxpayers were also willing to pay higher taxes to fund spending on public services..

1959-61

The next date when all four organisations and the press were researched in depth was 1959. By this point, the press and then, a year or two later, some Conservative politicians and researchers, had largely stopped raising the issue of popular opposition to tax levels, a shift which was particularly marked when compared to a decade earlier when there had been so much emphasis on popular opposition (albeit with little evidence). In the Conservative party some maintained the focus on opposition, but others were suggesting that people were more concerned about maintaining public services than cutting taxes.

It is not entirely clear what caused this shift in ideas in the press and the Conservative party. Although the standard rate of income tax had fallen slightly, the income tax system at this point was complex, with allowances also effecting rates. Recent estimates suggest effective income tax rates had not fallen for most people. Very little survey evidence was found for the period around 1960, but the Conservative Research Department conducted its own polling in the early 1960s indicating that people were more concerned about maintaining services than cutting taxes. Other surveys suggested support for increased spending over tax cuts, although perhaps particularly in relation to pensions. Conservative politicians and researchers’ increased access to, or interest in, polling might, therefore, explain why their perceptions changed.

Few reports of this, or other, relevant evidence were found in the press, but without access to detailed information on the tax system, journalists could have taken headline income tax cuts at face value. This could also have been reinforced by a decline in their own, and likely many of their social contacts’, tax liabilities – effective tax rates for those on higher incomes had reduced slightly by the end of the 1950s (the top marginal rate, for example, had been reduced from 97.5 percent in 1952 to 88.75 percent by 1959).

Whatever caused the change in perceptions among some Conservative politicians, there does not appear to have been a wider shift among the other organisations studied. There was far more continuity evident in the records of the TUC, FBI and Labour party, which continued to mention general opposition to tax levels and increases but combined with concern about fairness and support for spending on public services, as they had done a decade earlier.

The late 1960s

This change also seems to have been short lived. By the mid-1960s Conservative politicians and researchers, as well as some senior civil servants, were suggesting that opposition to tax was increasing and might soon become a major issue. This could have been driven by the press, which did emphasise popular opposition to tax slightly more around the 1965 Labour budget (which introduced new corporation and capital gains taxes for the first time) but press comments about popular opposition were still far less prevalent than they had been around 1950.

More surveys are available for this period, and, although of variable quality, perhaps suggest that support for higher spending fell through the 1960s (as spending increased under the Labour government) while support for tax cuts increased, but not if that meant cuts to services. Even by 1969 surveys suggested that cuts to services were more unpopular than tax increases. This survey evidence was not available until the end of the decade and so is unlikely to have driven the revived concern about popular opposition to tax in the Conservative party and among some in the civil service earlier in the 1960s. Conservative party polling suggested that tax was not a major issue for the public.

Discussions in the other organisations studied again remained fairly consistent. The FBI, and then from 1965, Confederation of British Industry (CBI), expressed their members’ concern about Labour’s 1965 tax reforms but did not fundamentally challenge them. Labour politicians and civil servants were concerned about opposition to the 1965 budget from wealthy taxpayers but, in general, their ideas about popular attitudes to tax remained consistent. So, while Conservative politicians and researchers, and some senior civil servants displayed concern about increasing popular opposition to tax in the mid-1960s, they appear to have been largely alone in this, and it does not seem clearly to have been based on new research or evidence.

What changed in the late 1960s and 1970s?

Although the late 1960s and 1970s have been cited by leading historians working on tax as the point when popular opposition to taxation started to increase markedly, evidence for this in the sources consulted was limited. A few isolated comments indicated that opposition to tax might have been increasing, but overall, discussions about popular attitudes did not seem to have changed significantly.

The TUC seemed slightly more concerned about opposition to tax rises around 1970 but did not suggest that opposition had increased and continued to emphasise the importance of fairness. Butler and Duschinsky suggested that changing attitudes among grassroots Labour activists drove increasing concern about opposition to tax in the party around the 1970 election but, if so, this appears perhaps only to have been informally expressed — it is not immediately evident in the archival record. Labour comments again demonstrated the consistent mix of assumptions about opposition to high or rising taxation along with concern about fairness and service provision.

Conservative politicians had evidence of extensive (though not necessarily increasing) opposition to the tax system among their most engaged activists through the Conservative Political Centre groups, but this does not appear to have changed their ideas about popular attitudes in the electorate. Neither party seemed to think that tax was particularly important to the 1970 election result, even though some polling did indicate that tax had risen up the list of priority issues for voters slightly.

Press emphasis on popular opposition to tax levels had increased again by the 1970 election and become more partisan, with right-leaning papers emphasising opposition far more than left-leaning papers. On the other hand, press representations of opposition still had not returned to the levels seen around 1950, and articles also expressed doubts about how attractive Conservative tax policies would be to voters.

There were some indications from polling that support for further expansion of public services was declining through the 1960s as spending rose, and a few individuals in the organisations studied thought that opposition to tax might be increasing. However, the survey evidence did not suggest that decreasing support for service expansion meant increasing support for tax cuts if that required spending cuts, and the comments found that suggested increasing opposition were isolated instances.

By the late 1970s there is more evidence that some individuals within the organisations studied thought, or at least stated, that opposition was increasing. Comments emphasising popular opposition to contemporary tax levels and further increases were prevalent. However, similar comments were common in earlier periods too, and statements suggesting a significant increase in opposition were still a small minority.

A note by the Conservative Taxation Policy Group (TPG), as well as a comment by its Chairman, David Howell, suggested that support for income tax cuts had increased because inflation had meant more people paying the standard rate of income tax. But most discussions found, including in the Conservative archives, suggested a view of attitudes consistent with earlier periods. Some Conservative politicians and researchers thought personal tax cuts would be popular, but not cuts on high earners or companies, which they expected to be viewed as unfair.

Some Labour politicians also seemed to suggest, less explicitly, that opposition had increased, and emphasised opposition to tax more in 1977 than other years. However, most Labour comments were, again, in line with previous discussions. The idea that opposition to tax would be, or had been, the deciding factor in the 1979 election did not seem to be prevalent in either party at the time.

Some civil servants appeared perhaps slightly more opposed to personal tax levels themselves around the 1976 budget, but their comments about popular attitudes had not changed. CBI officials increasingly suggested that their members were opposed to tax levels in arguing for its policy priorities, but their largely fruitless attempts to engage their members on tax policy did not suggest significantly higher opposition. And the TUC was communicating its members’ opposition to the current level of taxation but did not argue that this outweighed support for spending on public services or suggest that opposition had increased.

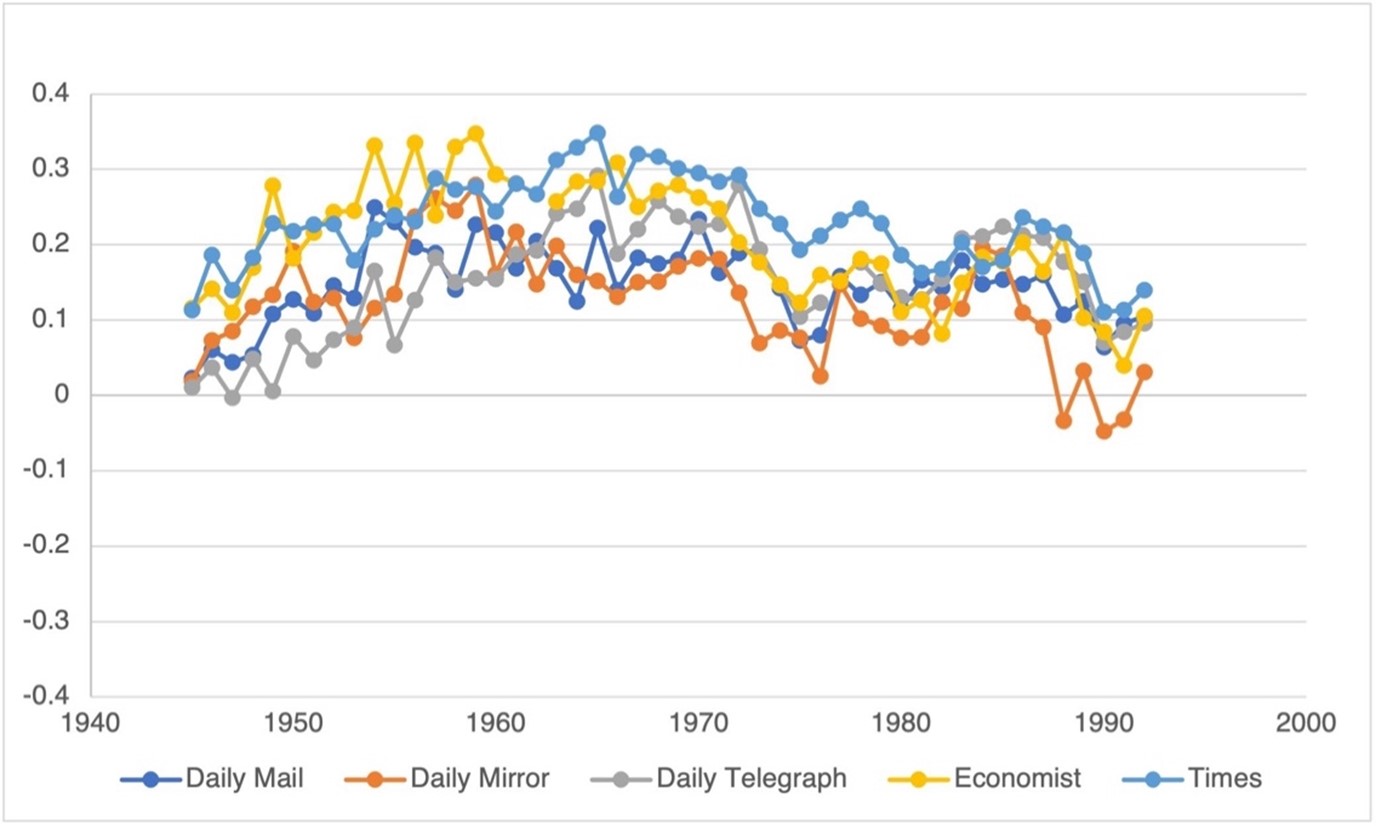

It was only in the press that a significant shift seemed to have taken place — popular opposition to tax was barely mentioned around the 1976 budget but was heavily emphasised by the 1979 election. Even this, however, was not unprecedented, and could as easily be seen as a return to the tone of press conversations about popular attitudes to tax found around 1950 as constituting any unprecedented change. This qualitative impression is supported by a sentiment analysis. Sentiment analysis is a natural language processing tool, in which a dictionary of positive and negative words is used to score text on how positive or negative it is. The graph below shows the mean score for each year for articles mentioning tax (excluding as far as possible company reports) from a selection of national papers. The scores were generally positive, although the more in-depth qualitative analysis found a huge number of negative articles (the drop in scores in the late 1980s is most likely related to the poll tax, which was excluded from this study). More interesting is the change in scores – which broadly became more positive through the 1950s, plateaued in the 1960s and became more negative again through the 1970s, but not, interestingly, more negative than they had been in the late 1940s, supporting the qualitative findings. In addition, while a few articles were found that implied that opposition might have increased, none asserted it explicitly, and most articles gave no indication of how they thought popular attitudes to tax might have changed – and none cited any quantitative evidence.

Sentiment analysis of articles referencing tax, mean yearly score 1945-92

Source: ‘Gale Digital Scholar Lab.’ Gale Cengage, 2020. Accessed on: 29 June 2020 at https://www.gale.com/intl/primary-sources/digital-scholar-lab.

The contemporary survey evidence does not suggest that popular attitudes to tax changed fundamentally in the 1970s either. Support for increased spending seems perhaps to have continued to decline but in 1979 there was still a clear preference for maintaining public services over tax cuts. Comments found which implied that opposition had increased were also almost exclusively confined, outside the press, to the period 1975-7. None were found in the lead-up to the 1979 election. While it goes against the accepted ideas of attitudes to tax in the 1970s, it seems, therefore, that the comments that implied opposition had increased might best be viewed as a response to historically high effective income tax rates, which peaked in 1977, rather than to the idea that attitudes to tax had changed fundamentally.

The later construction of a story about attitudes to tax in the 1970s

The idea that popular attitudes to tax had changed fundamentally in the 1970s was found, however, in press articles years later, in the late 1980s and early 1990s. In 1987 articles were divided about whether attitudes had changed before Thatcher came to power, resulting in her election, or after 1979, because of her policies. In 1987 the second option was far more common. By the 1992 election, however, this second idea had disappeared, leaving only the suggestion that opposition had increased in the 1970s.

Where this idea came from and why it emerged later is unclear. It was not supported by any survey evidence apart from one methodologically questionable IEA report published in 1979. It is possible that this could have been the source of this idea but there is no obvious reason why it would have still been influencing journalists’ views a decade after it was published. It does not appear to have come from academic studies. Although a few academic articles in the early 1980s did suggest that attitudes to tax had changed in the 1970s, others suggested they had not, and neither seem to have been widely reported in the press – either at the time they appeared or a decade later. Further research is needed to properly investigate the source of this idea that popular attitudes to tax changed in the 1970s. It does not, however, seem to have been primarily driven by, or based on, any credible or formal evidence of changing popular attitudes to tax.

Outside the press, no statements were found that suggested that opposition had increased during the 1970s. Although defeat in the 1987 and, in particular, 1992 elections seems to have increasingly convinced Labour politicians that there was widespread popular opposition to tax, even in 1992 this remained contested, with the importance of public services and fairness again emphasised in the discussions studied. Labour’s immediate assessments of the 1992 election defeat identified tax as only one of a range of relevant factors, with the linked, but separate, issue of economic competence likely the most important. TUC officials seemed slightly more convinced of opposition to tax increases but, in general, did not seem overly concerned about popular attitudes. Conservative politicians, civil servants, and CBI officials acknowledged opposition to taxation but, as previously, this was accompanied by the assumption that spending was equally, if not more, popular, and perceptions of fairness crucial.

Conservative researchers expressed some interest in evidence of popular attitudes to tax in the 1960s and 1970s but in general the organisations studied here did not often seem that interested in accessing evidence of popular attitudes. The TUC and CBI may understandably simply have been focused on representing their memberships. The political parties clearly were concerned about popular attitudes to tax but, despite this, the Conservatives for large periods, and Labour for almost the entire period leading up to the late 1980s, did not seem to be making significant efforts to obtain evidence of attitudes to tax – or if they were it is not evident in the archival record. When they did begin to have continuous reliable, independent survey evidence, from the annual British Social Attitudes survey from 1983 onwards, this evidence seemed generally to have been discounted in favour of personal impressions and interpretations of electoral results. The potential for bias in their ideas about popular attitudes was recognised on at least one occasion in the organisations studied; in discussing a survey that had been commissioned from NOP in 1965, looking at what kind of political language and phrases were most attractive to voters, Conservative researchers James Douglas and Peter Bocock wrote:

The answers more than confirm the impression already given by the survey, of an electorate more interested in the well-being of everybody (including the mediocrities) than in differential payment for ability … The results of this survey were frankly a surprise to both of us. It also gives one a rather unpleasant shock to realise that the way our instinctive judgments were off-target can, on the evidence of the survey, all too easily be explained by what one knows to be the bias in our own range of contacts:- too much middle-class, too much weight on men in their thirties and forties, overweighting of the home counties.

Little other evidence of similar self-interrogation was found in the organisations studied, and subjective beliefs seem often to have been given the most weight in discussions about popular attitudes to tax — politicians, journalists, and officials all seemed broadly confident that they knew what popular attitudes to tax were and did not need to consult research findings. This perhaps points to the importance of what was accepted as the ‘common sense’ view of attitudes to tax in elite social circles in shaping the discussions shown here, rather than quantitative evidence.

Implications for tax policy

- Popular attitudes to tax are almost certainly a constraint on tax policy but not in the straightforward way that often seems to be assumed and not clearly any more than they were in the immediate post-war period when tax rates were significantly higher than they are today.

- The national press is perhaps a greater constraint – not necessarily in its impact on popular attitudes themselves, but in its impact on elite political discourse and in contributing to, or reinforcing, the ‘common sense’ view of attitudes. Press statements about popular attitudes to tax over the period studied were frequent and rarely based on any clear evidence, sometimes running clearly counter to the evidence that was available.

- When trying to maximise popular consent for tax policy changes the experience of the second half of the twentieth century suggests that more attention should be paid to creating a persuasive overall narrative of why changes are needed. This would include the condition of public services, what the public sees as fair, and ensuring a decent level of public understanding of the changes that are being proposed, including by communicating to the public more clearly than is often the case now.

- Current perceptions of falling quality, or even a crisis, in public services would suggest, based on the historical trends in surveyed attitudes, that support for spending and tax increases will rise again, as happened between 2010 and 2017. Framing any proposed increases within the context of support for reviving and renewing public services and providing a clear narrative about the role of the state and the tax system in meeting current challenges, might be expected to increase popular support.