The UK Government’s strategy for digitalisation of the UK electricity network calls for a ‘smart and flexible energy system’, able to support ‘millions of low carbon technologies across Britain talking to each other’. But a report from the Renewable Energy Association claims that the UK network has fallen behind other countries in flexibility. This raises the question of what might be holding back the investment required to modernise the energy network.

The digitalisation of the UK telecom network three decades ago shows how the incumbent operator failed on that occasion to foresee that flexibility would generate more profitable revenue for the network itself. A newly flexible network encourages fierce competition between suppliers of equipment and services for exploiting network capacity, by for example linking zero-carbon generators to potential energy storage customers. A characteristic of embryonic competition is innovation. Innovation will lead to more efficient utilisation of network services, improving the network operator’s ‘top line’. It was a failure to recognise this potential in 1992 that threatened to derail the UK telecom network’s investment in digitalisation.

Three decades ago the UK telecom network was at an early stage of digitalisation. Computerized telephone exchanges were replacing electromechanical, and digital fibre-optic cables were replacing analogue terrestrial circuits, microwave dishes, and satellite links. The development of fibre-optic cables, which had gone from scientific curiosity to transmission technology of choice in only a decade, parallels the rapid advance of solar energy technology today.

When the Government privatised British Telecom in 1983, it agreed to allow only one competitor (Mercury) for the next 7 years. By 1990, at the end of that ‘duopoly’ period, Mercury had gained only four per cent market share. It seemed likely that the Government would soon licence other operators to increase the pace of competition.

Alarm bells rang at the Department of Trade and Industry after it commissioned a report into the practicalities of interconnecting more rival operators to the existing BT network. The report argued that BT’s decision the previous year to reduce its investment in new digital exchanges would make it harder for new market entrants to use BT’s network. The report recommended that the Government regulate BT’s capital expenditure with the object of making the network more flexible. This would be a dramatic addition to the price control (‘RPI-X’) regulation that the UK had been pioneering. The report pointed out that BT was the only one of the world’s privatised telecom operators whose capital investment plans did not need regulatory approval. BT was in fact significantly cutting back on exchange digitalisation: capital expenditure on telephone exchanges fell from £952m in 1989/90 to £545m in 1992/93. BT cited a change in emphasis from digitalisation to improving customer service.

The regulator, Oftel, reviewed the RPI-X formula every five years, adjusting the value of X in a way that would share the benefits of new technology between BT’s shareholders and customers. In mid-1992 Oftel published the results of its latest review: Future Controls on British Telecom’s Prices. Readers were surprised to see a paragraph on ‘investment expenditure’, because the UK had made a choice of price control regulation instead of the US-style supervision of investment and ‘rate of return’. In the new paragraph, Oftel said that the operator must, before the next 5-year review, have given 99% of the population access to a digital exchange and must have installed 3.3 million km of optical fibre.

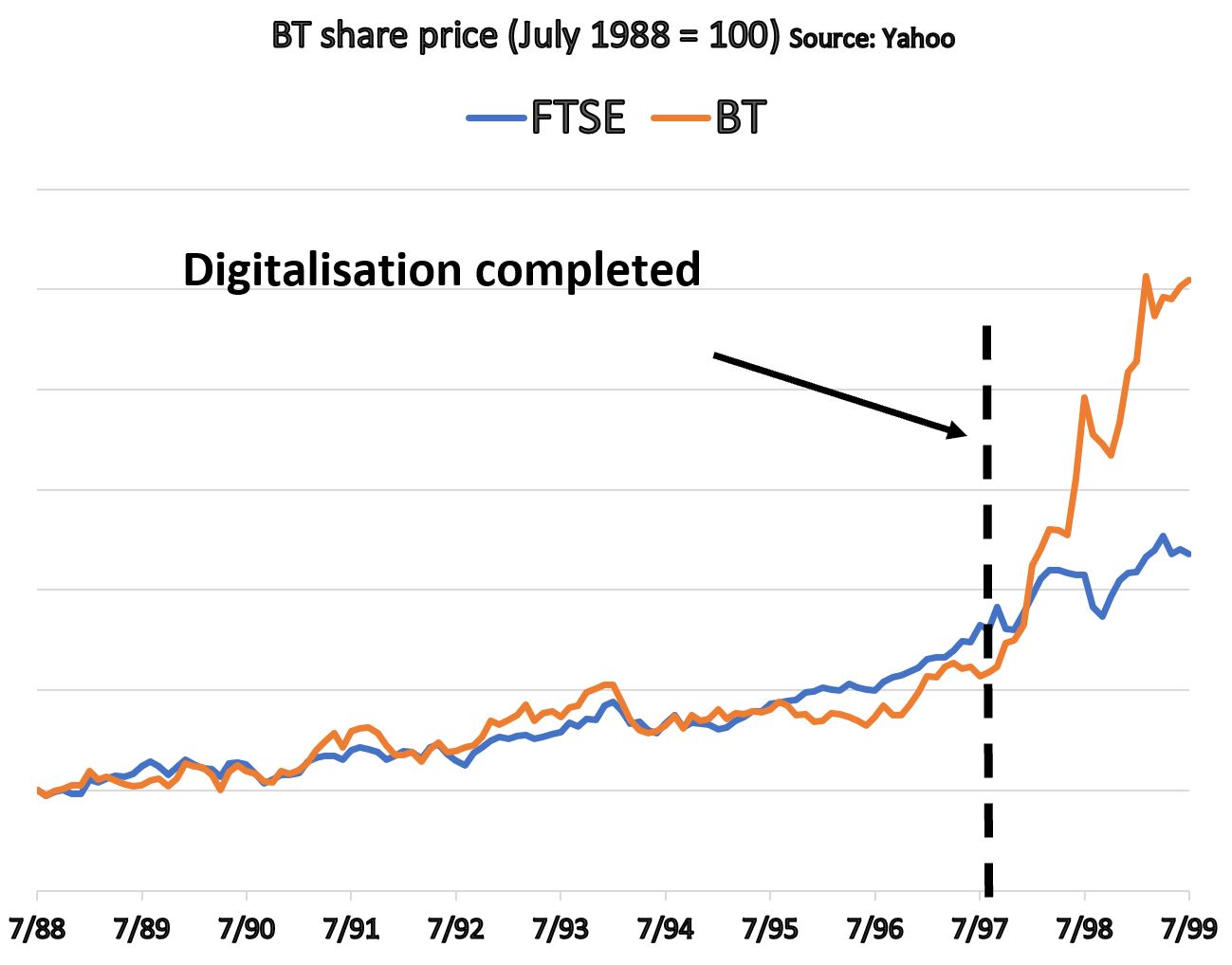

BT’s shareholders stood to benefit from the reduced maintenance costs and additional revenue from new features of digital exchanges. Oftel would have considered these benefits when setting the new price control formula at RPI-7.5. However, the lesson of 1992 for the electricity companies does not lie solely in these more predictable shareholder benefits, but in the unforeseen wealth that accrued to BT shareholders following that company’s reluctant acquiescence to Oftel’s new digitalisation deadline.

After BT had met the deadline in mid-1997, the company’s share price shot up, rapidly outpacing the FTSE 100 and BT’s previous performance. Oftel had not factored in that amount of growth when calculating the price formula for the period. The unpredicted growth came as external players took advantage of the network’s new flexibility.

Although the network duopoly was ended by 1997 and rivals to BT appeared, venture capital flowed to the providers of mobile telecom and internet services. These businesses had been straining at the leash, driven by competition between them but constrained by limited connectivity. After BT completed its digitalisation, mobile operators had no wish to build a rival to BT’s network for connecting up their base stations because they could use the excess capacity available in BT’s expanding fibre network at marginal prices. In 1992 only one per cent of UK households had a mobile phone; when the digitalisation deadline had been met it was sixteen per cent, and in the next five years, with full network flexibility, the UK became one of the fastest-growing mobile markets in the world.

So why did BT put up a strong resistance to accelerated digitalisation? The Financial Times Telecom Markets newsletter reported at the time that BT ‘reacted angrily to Oftel’s suggestion that it should meet a number of prescribed investment targets’. BT claimed that Oftel was acting outside its remit and was restricting the freedom of BT managers to manage. Norman Tebbit, who as Secretary of State for Trade and Industry had privatised BT and who was now a director of the company, told its staff that Oftel was over-regulating BT and that the Director General of Telecommunications was seeking popularity by attacking the company. The Director General made clear in turn that although he had discussed the new regulation with BT in advance, it was anything but a ‘suggestion’. He wrote ‘I do not believe that regulations should be settled by negotiations between the regulator and regulatee. If BT is unable to agree to my proposals, I believe that the issues should be referred to the Monopolies and Mergers Commission.’

BT’s Chairman announced at the company’s AGM that it would not be in BT’s interest to have the company investigated by the MMC. He perhaps had before him the prospect of suffering the same fate as US telecom operator AT&T, the biggest company in the world, which the US Justice Department had broken up in 1984 for abuse of monopoly.

BT’s strong resistance to a bold new form of regulation by Oftel, which in fact brought a windfall to its shareholders, was probably due to a mindset that also exists among privatised electricity network operators today. BT’s long history of monopoly gave them no insight into the ability of external competition to create innovative uses for its network. BT could not imagine, much less predict, the new and profitable demands that would be placed on a more flexible network by what had until then been known as Value Added Services or Customer Premises Equipment. With a flexible network, these previously unexciting businesses would morph into the giant internet and mobile services industries typified by Google and Apple. The capital investment required of BT to create the flexibility to support all these businesses and their customers was immense. But it was not simply a cost item; it was a profit opportunity well-matched to BT’s core competences and the availability of risk capital.

It is hard to detect any awareness of this telecom success story in the Government’s and Ofgem’s digitalisation strategy for the electricity network. The strategy lists as its first objective ‘decarbonising the energy system at least cost to consumers’. Cost reduction is therefore the goal and the 2050 net-zero target, not profit, is the motivation. This seems odd in a digitalising industry where demand is strong, new sources and uses of sustainable cheap energy are available, and innovation is producing more. It contrasts strongly with consumer experience of telecom digitalisation. Telecommunication has not shrunk as a proportion of consumer expenditure: it is now seen as a way to save money elsewhere. Apple did not make its smartphone network flexible enough to support third-party apps with the aim of reducing its customers’ telecommunications costs.

The published digitalisation strategy proposes mechanisms to improve today’s planned energy economy rather than to move towards an ‘energy internet’ that would connect buyers and sellers of innovative energy products. The strategy relies on “the digitalised exchange of data to facilitate an energy system which can accelerate, automate, plan, and anticipate processes far better than at present”. This sounds like a recipe for a planned economy, with data collection being the principal benefit of digitalisation. The strategy still promotes the need for consumers to ‘switch’ between suppliers, implicitly assuming that a consumer will have an exclusive contract with one supplier for all types of electrical energy, however it is generated.

The most serious obstacle to innovation in energy products is that regulations require intermittent power generation to be paired with standby generation capable of fast start-up in case there is a break in supply. As the UK Government’s Climate Change Committee puts it “wind and solar generation can change substantially over periods of just a few hours, requiring non-renewable plants to be held in reserve to meet any sudden shortfall in supply.” At best, this expensive and dirty standby capability consists of gas-fired generation whose cost is added to the very low cost of the intermittent energy. This pricing handicap is referred to as ‘the cost of intermittency’ but is really the cost of converting the cheapest forms of electrical power into the traditional ‘firm’ or ‘baseload’ power which is all that the non-digitalised grid can handle. It is a grid that is designed to deliver ‘one size fits all’ power, just as the pre-digital telecom network was designed to deliver only ‘POTS’ – Plain Old Telephone Service.

As Professor Sir Dieter Helm points out, the result of the standby regulation is that “The gas and electricity price paths match each other remarkably closely in the UK”, adding that this is illogical: “in a system with lots of zero marginal cost generation, the price of electricity for all the [different forms of] electricity generation should not equal the spot price of gas.”

An important new goal for a digitalised grid should therefore be the commercialisation of intermittent power at lower market prices. The Climate Change Committee recognises that there are many commercial applications of cheap intermittent power, including charging batteries and creation of zero-carbon hydrogen fuel. There are more speculative uses, such as supercomputing and ‘manufacturing only while the wind blows’. To ensure that expensive demand for baseload power has first call on intermittent supplies during demand peaks, the digitalised grid will need to recognise that the cheapest power is not only intermittent but must also be interruptible. Mobile telecom service is both, due to incomplete coverage, but has enormous value nonetheless.

The viability of Innovative applications for different grades of intermittent electrical power cannot be reliably assessed or devised simply by analysing data produced by the current strategy for digitalising the current network. These applications can only be developed by risk capital investing in new products in an open network ecology with low barriers to entry and exit, like the late-1990s telecom network. Hence the urgency. As the House of Lords Select Committee on Economic Affairs recommended in its response this year to the shortcomings of the Government’s Net Zero plan:

[The Government will need to] Establish appropriate market mechanisms and incentives to encourage investment in low carbon technologies;

Could the UK economy one day survive and grow using only intermittent electrical energy (wind, solar, tidal, and stored energy derived from those sources)?

In 2018 the UK already derived nearly a quarter of its electrical power from wind and solar generation, and the Government proposes to increase offshore capacity by a factor of three, and onshore by a factor of two, by 2030. The country will face a challenge in absorbing so much intermittent energy. The challenge is exacerbated by the relative expense of exporting surpluses compared to other wind-intensive countries with land borders. ‘Constraint payments’ to wind farms have decreased in recent years as the grid has increased transmission capacity to the less-densely inhabited areas where wind is plentiful. As the Climate Change Committee points out, however, “[w]ith high penetrations of intermittent renewables there are likely to be periods where output is in excess of demand. This output would effectively be wasted and have no value.” The answer would appear to lie in boosting demand, and the Committee does in fact foresee a doubling of demand for electrical power by 2050 due partly to electric vehicle charging and production of hydrogen fuel gas by electrolysis.

It should be borne in mind though that even zero-carbon energy could impair the planet’s energy balance if greenhouse gas has not been sufficiently reduced. Energy cannot be destroyed; surplus electrical energy could be converted to kinetic energy and expelled from the planet in the form of a projectile, as recent experiments have shown.

Some of the possibilities, including an economy based purely on intermittent energy like the first industrial economy pioneered in Britain using sail-powered shipping and water-powered mills, may seem like science fiction. They do not seem so far-fetched to those old enough to see how technology has radically altered our way of life over the last 50 years. An economy without the need to maintain the capacity for ‘firm’ or baseload energy supplies would certainly remove the most dangerous geopolitical and environmental risks that we run as a result of our dependence on fossil fuels

New technology is causing the energy industry to experience a ‘maturity reversal’ in which products are de-commoditised and innovation flourishes, as in a start-up business.

The example from the digitalisation of the telecommunications network shows that monopolistic enterprises cannot be expected to foresee the shareholder benefits of competition.

Industry regulators should follow the example of the telecommunications regulator of the 1990s and use ‘tough love’ to ensure that network operators deploy technology that facilitates flexibility and reduces barriers to entry and exit.

The Slowing Modernisation of the UK Telephone Network. Report by Arthur D. Little Ltd to Department of Trade and Industry, 10 July 1990

Future Controls on British Telecom’s Prices: A Statement by the Director General of Telecommunications. Oftel, June 1992

Telecom Markets newsletter, Financial Times Business Enterprises Ltd., 1992

Net Zero - Technical Annex: Integrating variable renewables into the UK electricity system. In Net Zero – Technical report, Committee on Climate Change, May 2019

Energy Transition Readiness Index, Renewable Energy Association, 2019

Delivering on the Potential of Flexibility, Association for Decentralised Energy, 2020

Digitalising our energy system for net zero, Department for Business, Energy, & Industrial Strategy, 2021

Sign up to receive announcements on events, the latest research and more!

We will never send spam and you can unsubscribe any time.

H&P is based at the Institute of Historical Research, Senate House, University of London.

We are the only project in the UK providing access to an international network of more than 500 historians with a broad range of expertise. H&P offers a range of resources for historians, policy makers and journalists.