Introduction

This has been the year in which 'cuts' became the mainstay of political rhetoric. The leaders of both main Opposition parties, David Cameron for the Conservatives and Nick Clegg for the Liberal Democrats, made the reduction of Britain's national debt the centrepiece of their party conference speeches in the autumn of 2009. Mr Clegg even referred to the need for 'savage' reductions in public spending. Even Gordon Brown, who for most of his time as Chancellor of the Exchequer and Prime Minister made the distinction between 'Labour investment' and 'Conservative cuts' the defining choice in British politics, accepted that there would have to be reductions in public expenditure. The purpose of this paper is twofold. First, it will attempt to place this urgent question of Britain's national debt and current public sector borrowing in a historical context. It will ask: is the stock of UK state debt now very high as against what it has been in the past? And, secondly: is it actually excessive by comparison with that of other nations? The paper will then move on to examine the record of various governments in cutting public spending since 1945. It will discuss the 'lessons' policy-makers should draw from the control of public borrowing in that period, before concluding with a short discussion of those techniques that are most likely to lead to longstanding reductions in the current public sector deficit.

Theory, history and British public sector debt

The first point to note about public sector debt is that it is quite unlike household borrowing. The ability of governments to borrow is much greater than that of private citizens, and they may do so much more cheaply than individuals. Since they represent nearly the entirety of economic activity within their borders, they are unlikely to be completely unable to pay – unlike the international bankers and City of London financiers who have dominated economic policy since the 1980s. The British economist John Maynard Keynes, newly fashionable since the implosion of world financial markets began in 2007, understood this well. He would undoubtedly have approved of the recent policy of 'quantitative easing', by which the Bank of England has added to the money stock by buying up government debt. As he put it in his General Theory in 1936:

Unemployment develops… because people want the moon; men cannot be employed when the object of desire (i.e. money) is something which cannot be produced and the demand for which cannot be readily choked off. There is no remedy but to persuade the public that green cheese is practically the same thing and to have a green cheese factory (i.e. a central bank) under public control.

Similar reasoning explains how successive governments could run a consistent, though small, current deficit in the post-1945 period, while still paying down their debt very rapidly. The long time-spans involved, given that public debt was often issued on thirty- or forty-year terms, allowed even a small amount of inflation to eat away at the value of indebtedness over the medium term. Even constant additions to the stock of total borrowings were also dwarfed by rapid economic growth, as in the 1950s and 1960s, and tax rises – most notable in the late 1960s and 1970s.

Historical parallels with our present situation

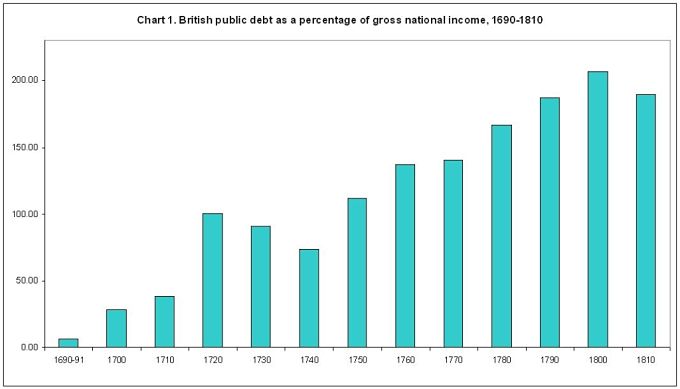

Statistical evidence, as well as theory, can help us with three vital questions. How high is British debt in relation to the historical record since the creation of the public debt in 1690? How high is it in relation to other countries' borrowings? And what is the likely situation going forward? Charts 1-4 help answer this question. Charts 1 and 2 lay out the historical record since the seventeenth century. They demonstrate that British public debt has been consistently higher than it is today, though usually to pay for wars. Neither chart contains statistics that are quite analogous to today's figures, for a variety of methodological reasons, but they demonstrate that, in general, the UK has consistently borne very high levels of government indebtedness. The eighteenth century saw particularly large increases in the size of the armed services, and each successive conflict saw public debt peak at a new high. Chart 1 reveals the detail, with the War of the Spanish Succession (1701-14) forcing the National Debt up to 100 per cent of national income, and the Seven Years' War (1756-63) and the long struggle with Revolutionary and Napoleonic France (1793-1815) pushing the figure higher still, to 140 and then to over 200 per cent of national income.

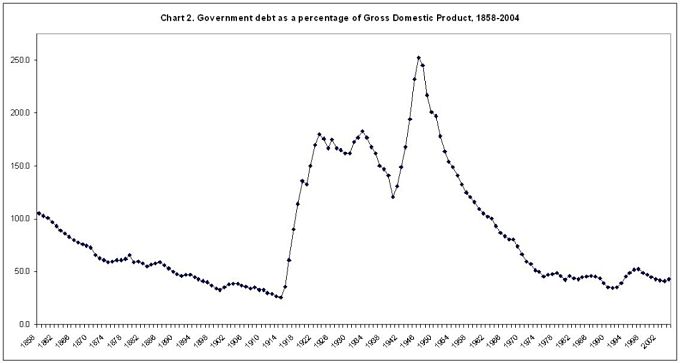

However, even in an age when there were no 'public services' to speak of, not all state spending went on the military. Even during the Seven Years' War and the War of American Independence, military spending amounted to 71 per cent and 61 per cent of government spending respectively. The two World Wars of the twentieth century similarly required the UK to borrow enormous sums from the US and the Empire-Commonwealth. These pushed public sector indebtedness back up after the long era of Victorian peace and retrenchment, before the fast growth of the 'golden age' between the 1950s and 1970s brought the figure back down again (see chart 2).

Chart 1

Chart 2

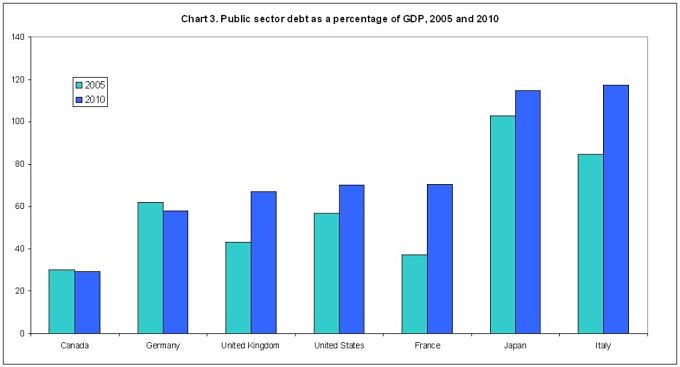

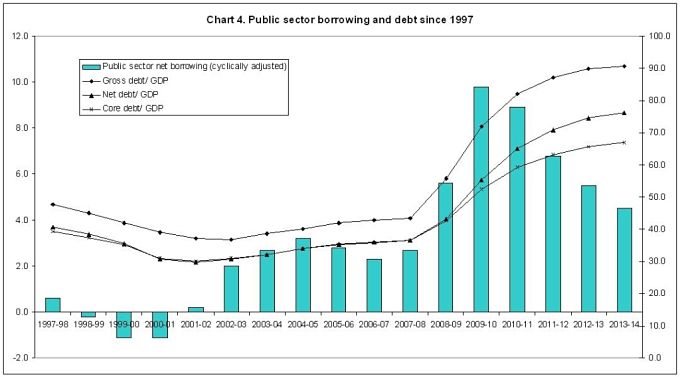

Chart 3 represents a comparison between British and other developed countries' state liabilities. This shows that the British state is actually bearing a relatively low debt burden when compared to those of other states – the opposite of the situation that prevailed throughout most of the post-Second World War era up to the 1980s. Though much higher than the arrears of resource-rich Canada, Britain has only marginally higher public borrowings than Germany, and slightly less than the USA and France. State debt is also much lower than the comparable figures for Japan and Italy. A period of debt repayments between 1997 and 2001, clearly noticeable in chart 4, helps to explain this situation. As Chancellor, Gordon Brown followed Conservative spending plans for the first two years of Labour's first term, and when he did authorise higher spending, Whitehall departments moved only slowly at first. Chart 4 uses 2009 Budget figures to project a possible scenario going forwards to the financial year 2013-14. Official projections predict that the total stock of public debt will rise to 90 per cent of GDP – figures that have not been seen since the early 1960s – but then move onto a falling, rather than a rising, trend. It must also be noted that 'net' debt – taking into account the Government's income – will peak at a less alarming 76 per cent. More importantly in terms of the present policy debate, 'core' debt – excluding the bank bail-outs of 2007-2008 – will peak at a much lower level, around 67 per cent. Although the near-collapse of the banking sector has hit Britain particularly hard, some of this money will eventually return to the Treasury when the banks return to private hands. If we exclude that operation – a series of spending decisions that may have saved the international financial system – there is no sense in which basic public spending is 'out of control'.

Chart 3

Chart 4

The remaining requirement for cuts

None of this evidence demonstrates that UK governments can ignore public sector debt as it stands. It may be relatively low by international and historical standards, but the last two financial years have seen it rise very quickly – certainly much more quickly than that of other comparable states, as chart 3 demonstrates. Treasury forecasts assume three per cent economic growth for the next three years up to 2013-14, an optimistic (though not impossible) assumption. Government revenue from returning the banks to the private sector is very uncertain. The National Audit Office has estimated that total government liabilities, including loan guarantees, insurance and liquidity support, might add up to a vast £850bn. This sum would amount to more than half Britain's GDP on its own. But it is worth noting that the uncertainties involved in policy-making might work to help, as well as hinder, government finances. Population forecasts from the 1960s, for instance, turned out to be far too gloomy about the numbers of dependent old and young people in the population. If little more support is drawn on, government spending on the bail-out might not amount to much more than the £50bn the government quoted in spring 2009.

There are, even so, myriad other reasons why it might be risky simply to leave public debt where it is planned to be by 2013. Public sector pension liabilities are not included in these figures, and although it is in the power of central government to increase contributions to these funds or to reduce their generosity, they will on present assumptions rise very rapidly. Most of the periods which have seen public debt soar over the last three centuries have involved total war against an external aggressor, rather than an economic crisis triggered by the collapse of financial institutions. As Mark Roodhouse has noted in his 2007 History & Policy paper, Rationing returns: a solution to global warming?, creating a sense of 'national emergency' among a peacetime public would be very difficult indeed. Such an ethos would, however, be necessary if growth assumptions are undershot and public debt continues to rise at the present rate. The electorate's capacity to bear financial pain might be severely tested if the public had to meet the costs of a global warming 'emergency' at the same time.

Econometric analysis of the UK experience between 1920 and the mid-1990s demonstrates a mild, though significant, 'crowding out' effect, in which high state borrowings may restrain private borrowings and thus curtail increases in the private capital stock. Even though Keynes was strongly in favour of government spending in periods of deficient private demand, he understood very well the related phenomenon of 'psychological crowding out': the panic that might be caused by the perception that government borrowing was rising far too quickly. Finally, evidence from the past three hundred years demonstrates that there is a relatively strong relationship between periods of high government debt and rising interest rates – a relationship which seems to have grown rather than weakened in strength since the 1970s. There is already some evidence of this effect in action today, for the UK government is being forced to offer higher rates on ten-year bonds than the French or American governments. So there will indeed have to be reductions in public spending, and it would be prudent to go further than present Budget predictions, to create a margin of safety.

The record since 1945: tax rises

So there probably is a need to find further savings from planned programmes, and we can turn to the historical record for clues as to policies that might work. In the post-war era, there have been three notable periods of public expenditure reductions and debt reduction while the economy was actually growing: Labour struggled to right the external balance of payments via cuts in home consumption in 1968-70, and then to pay back its 1976 borrowings from the International Monetary Fund (IMF) in 1976-78, while the Conservatives attempted to right the damage caused by the 1990-92 recession over the years that followed. Each episode carries lessons for policymakers today.

The first point to make is that all three periods involved significant rises in taxation. The 1968 Budget increased Labour's Selective Employment Tax on service industries, introduced a 'special charge' on investment income, and hugely increased a range of indirect taxes, for instance on beer. Taxes went up overall by £923m in contemporary prices.

The first crisis package of 1976, announced in July of that year, cut £1bn from public spending over the following year, but also added a further two percentage points to employers' National Insurance contributions, which would reduce government borrowing by another £1bn in 1977-78. Later in the year, when the financial markets had judged those measures woefully inadequate, the mix was rather different: another £1bn of cuts, plus the sale of £500m government shares in British Petroleum. But the fact remains that nearly one third of the entire budgetary tightening was made up by tax increases, which were by now pushing the limits of political acceptability among the public and employers. In particular, marginal rates of income tax (which in 1976 reached 83 per cent for very high earners) were felt to be particularly onerous – to be borne, perhaps, in the midst a financial crisis, but not to be endured on any permanent basis.

In 1993 Norman Lamont imposed Value Added Tax on fuel and power, froze income tax allowances, increased National Insurance payments and cut Mortgage Interest Tax Relief. Together these measures reduced the Public Sector Borrowing Requirement (PSBR), which in 1993 stood at £35bn, to the tune of more than £6bn by 1995-96.

The record since 1945: the Cabinet is critical

Another shared and striking fact concerning these exercises was the role of the Cabinet, which was paramount during each wave of public sector spending restraint. It is quite clear that securing agreement at the apex of government was a prerequisite for success in the atmosphere of departmental and political competition that such exercises engender. In 1968, Harold Wilson asked the Cabinet to discuss these issues in their entirety, not only so that Ministers would talk themselves out, but to force them to consider cutting cherished social policy aims and defence expenditure in the same discussion. The raising of the school leaving age to sixteen was postponed and prescription charges re-imposed. Ministers also made the decision to save money by pulling out of Britain's 'East of Suez' defence role in Asia and Australasia during the early 1970s, in contrast to Gordon Brown's recent commitment of more British troops to Afghanistan. Each member of the Cabinet was asked for his or her vote in each case. Tony Benn, then Minister of Technology, observed that it was a notable achievement to hold most of the Cabinet together:

'Harold Wilson [was]… confirmed in his view that you couldn't spend more on defence than you could afford and at the same time accept some social service [had to] accept cuts. So everybody had to compromise.'

James Callaghan, confronted with a sliding pound and the arrival of an IMF team in 1976, used similar techniques. Denis Healey, Callaghan's tough and resourceful Chancellor, recalled that:

'the consummate skill with which he handled the Cabinet was an object lesson for all Prime Ministers. His technique was to allow his colleagues to talk themselves to a standstill in a long series of meetings, and then to invite the dissenters to put forward their alternative.'

Not surprisingly, the alternative to reducing borrowing – basically, a siege economy – received short shrift at this point.

Reforms to the public expenditure system early in John Major's government made collective consideration in Cabinet easier than it had been before. The inauguration of a joint spending and taxation Budget in the autumn, rather than separate revenue-raising and spending announcements in spring and autumn, allowed the Cabinet to look at the whole picture. The presumption that the Cabinet would stay within overall spending limits also encouraged the discussion of priorities.

Episodic attempts to cut spending, by slashing large infrastructure projects or placing faith in administrative solutions, have had less success. Labour learned both lessons on returning to office in 1964. The party attempted to cancel the supersonic Concorde project in civil aerospace, and to bring in a 'star chamber' which would judge Ministers' spending bids in a neutral manner. Neither initiative stood much chance of success because of vested departmental interests, the fear of political opprobrium or, in the case of Concorde, French legal action. Put simply, Ministers have to choose collectively the programmes they want to abolish or defer. Attempts to short-circuit that process with singular, 'representative' cuts, or through bureaucratic means, are unlikely to work.

All of these long periods of tough decision-making ended with state borrowings far below their initial position, and undershooting prior forecasts. The Wilson government's brake on public spending acted particularly rapidly. By 1970 the Government had built up an enormous surplus, and had far overshot its intentions in this respect. Callaghan saw the PSBR fall from nine per cent of GDP in 1976-76 to less than four per cent in 1977-78 and the government only had to claim half the credits the IMF had extended to it. The PSBR declined from eight per cent of GDP in 1992-93 to five per cent by the time New Labour took power in 1997. Given the relative success of previous initiatives, with their mixture of tax rises, collective responsibility and above all sense of politics as a set of actual choices for which Ministers accepted collective responsibility (and could explain), it might be as well for Ministers and officials to study these episodes in depth.

Conclusions: four myths

Four dangerous myths have gained a pernicious hold on public policy debate in the last few months. These are, firstly, that British public debt is at an unprecedented and unsustainable level. As we have seen, debt has been higher than its 2009 levels at many points during modern British history. The real 'lesson' we should take from British history is that public sector debt is now at levels that should elicit concern, but not panic. The second myth that must be challenged is that governments must slash spending, right away. Recent history repeatedly shows that the combination of background inflation, resurgent growth, tax rises and the establishment of a sound plateau for public spending are much more likely to be effective over the medium term. A third myth is the idea that the public finances are 'out of control', and particularly that the money borrowed has been wasted. On the contrary, there have undoubtedly been real and sustained improvements in public services, gains that should not now be thrown away with over-hasty cuts. Reducing the rate of public spending increases will, however, still be important over the next few years. But the fourth set of misconceptions, which leads politicians to feel the need to display an exaggerated 'toughness', are likely to frustrate rather than facilitate such efforts. Holding the Cabinet together, eschewing technical or immediate solutions, raising taxes, and accepting that gross government spending will actually continue to rise, will be essential if the expansion of state borrowing is to be reversed. Simply shouting about 'cuts', still less implementing 'savage' reductions, will not do.